NASHP’s Hospital Cost Tool (HCT) includes many data points to help state officials and other payers understand more about hospital costs and their relationship to prices for patient care. The tool uses hospitals’ Medicare Cost Report (MCR) data, the same source used to inform Medicare’s reimbursement for care services.

The HCT and a health system’s Audited Financial Statements (AFS) are distinct tools that provide different information. Specifically, because the HCT utilizes MCR data for individual hospitals, and the AFS reports data across entire health systems, the operating margin (and other measures) within each are often not aligned. Using the HCT and the AFS together, with their different data, however, can provide a more complete hospital cost and health system financial overview.

AFS versus HCT

AFS is an independent, objective, and comprehensive evaluation of an entire organization or company’s financial records prepared by a certified public accountant that ensures adherence to Generally Accepted Accounting Principles (GAAP) or Governmental Accounting Standards Board (GASB) and professional auditing standards. AFS is an excellent resource to understand a health system’s financials with information reported and attested to by the entity.

However, parsing out individual hospital financial details from the larger system is challenging and is not the intent of the AFS. The AFS is meant to share how the overall health system is performing financially by examining its consolidated revenues, expenses, and overall cash flow from its multiple, varied sources. For instance, entities providing loans and bonds require this level of financial insight before investing.

Hospitals submit MCR data to the federal government annually (also with signature and attestation) which identifies individual hospital costs, charges, and revenue. The Centers for Medicare and Medicaid Services (CMS) use MCR data to establish reimbursement rates for patient care covered by Medicare. Hospitals use the MCR data to understand trends in inpatient and outpatient costs in absence of a cost accounting system, identify strategies to improve financial performance, determine cost center profit margins, and identify strategies to improve financial performance.

NASHP’s HCT uses MCR data to highlight individual hospital costs that are not readily accessible through other sources. The tool seeks to provide state officials and other health care purchasers an explanation for how individual hospital costs relate to charges and ultimately, the prices paid by health plans, employers and importantly, consumers. In providing measures throughout the HCT, NASHP considers the MCR instructions for reporting specific data points and follows national accounting standards.

HCT Definition

“Operating Profit or Loss” is defined as net patient revenue (reported from a hospital’s accounting records) minus Hospital Operating Costs, which is defined as “portion of hospital expenses (inclusive of all services) related only to hospital patient care and eligible for reimbursement per Medicare federal regulations, sometimes referred to as Medicare Allowed Costs.”

Key Points of Differences

- The HCT operating margin measure shares the profit or loss for providing hospital patient care only considering Medicare reimbursement rules.

- Medicare reimburses hospital costs, both in- and out-patient services, separately from physician reimbursement. Medicare hospital reimbursement includes payment for certain hospital medical professionals, i.e., emergency and intensive care physicians, but a specialty physician bills and is paid separately.

- Given the Medicare reimbursement rules, the MCR reporting instructions, and the goal of the HCT to share the hospital costs for providing patient services, NASHP’s calculation includes specific expenses from MCRs, plus others such as home office and related expenses. But it removes others, for example:

- Professional physician costs, as they are billed to Medicare separately

- Private physician offices

- Advertising

- Cafeteria

- Gift shop

- The AFS calculations for operating margin are not dictated by Medicare’s hospital reimbursable costs. They include broader expenses and revenue across all the system owned entities, and do not provide detailed cost data, for example:

- Other Operating Revenue

- Salaries, wages, benefits

- Joint Venture financial transactions

- Equity earnings of subsidiaries

- Contract services for all entities

- Interest expense for all system debt

- Unrealized gains (losses) on investments

- Other property fees and leases, etc.

Comparing Report Details

As previously noted, the AFS provides the financials for all affiliated entities or the health system, not just an individual hospital. And the HCT shares cost, charge, utilization, and revenue data for individual hospitals as reported on their MCR. Therefore, the measures cannot easily be compared when assessing details for a system and an individual hospital.

In summary, both the AFS and the HCT are helpful tools to provide valuable financial information on health systems and hospitals. The HCT focuses on individual hospitals and use MCR data, which are public, annual reports submitted by hospitals to the federal government to inform Medicare reimbursement on patient care. Patient care is critically important to all purchasers, but prices for that care are a key factor in driving up health care costs, which states and employers want to understand.

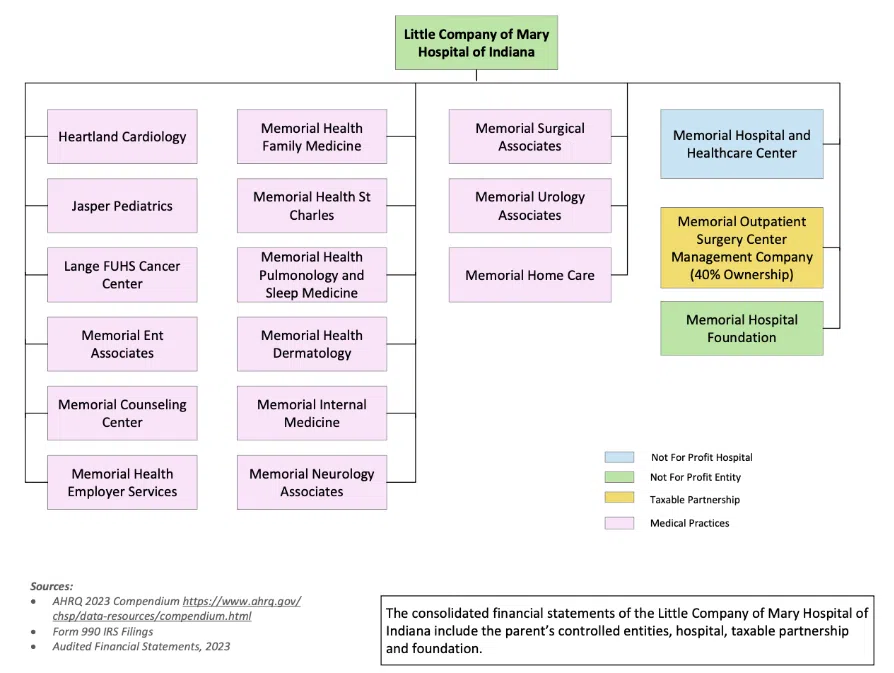

Sample Use Case

In 2023, the Memorial Hospital and Health Care Center in Jasper, Indiana, was a single hospital within the Little Company of Mary Hospital of Indiana – a health system. However, according to the Agency for Healthcare Research and Quality’s (AHRQ) Compendium of U. S. Health Systems, 2023, the system also included 15 medical practices, an outpatient surgery center management company, and a foundation. (See the organizational chart below.)

The 2023 AFS, representing the entire Little Company of Mary Hospital system, shows a negative operating margin. However, the 2023 HCT’s operating margin for the hospital in Jasper, Indiana, which considers Medicare’s reimbursement rules, is significantly higher at approximately 40 percent.

The AFS shares how the hospital’s financials are interwoven with its system affiliates, and the HCT provides insight on the hospital’s profit/loss for providing patient care. According to the HCT’s data the hospital (noted below in blue on the organizational chart) is covering its costs for providing patient care with a profit, but the AFS indicates the system’s revenue is not covering its expenses.